Table of Contents

ToggleIntroduction

Few doctrines have had as long-lasting and revolutionary an impact in the ever-evolving field of corporate law as the Doctrine of Ultra Vires. This doctrine, which has its roots in the fundamentals of company law, protects the interests of creditors, shareholders, and the general public by making sure that a company’s actions stay within the bounds set forth by the law. With the help of significant cases that have influenced its evolution, we will examine the definition, applicability, significance, and judicial interpretations of ultra vires in this blog.

Understanding the Meaning of Ultra Vires

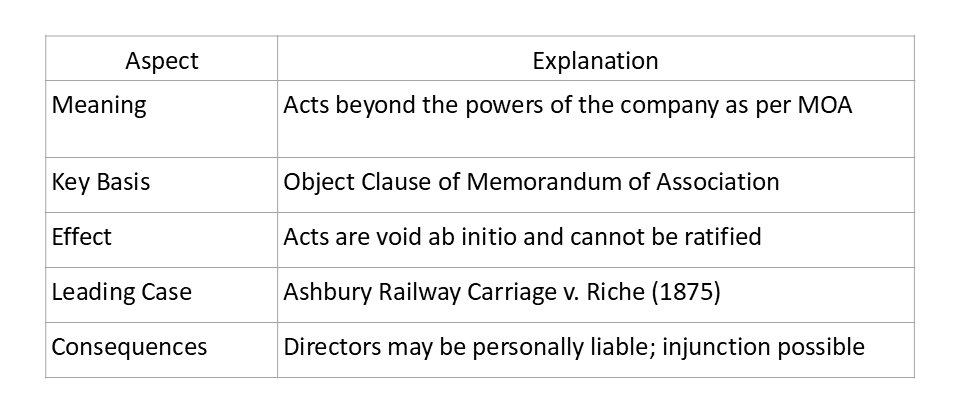

Ultra vires is a Latin phrase that means “beyond the powers.” It describes actions carried out outside the parameters of the authority and goals specified in a company’s Memorandum of Association (MOA) in terms of company law. Even if all shareholders approve of a company’s actions, they are still considered null and void.

The company’s constitutional charter is contained in the Memorandum of Association (MOA). It details the company’s name, capital, liability, registered office, and—most importantly—the objects clause, which describes the range of its operations. This objects clause is at the heart of the ultra vires doctrine.

To put it simply, a company is said to have acted ultra vires—beyond its powers—if it engages in an activity that deviates from its declared goals.

Origin and Objective of the Doctrine

The theory evolved as a legal tool to safeguard creditors’ and investors’ interests in the 19th century. It made sure that a company’s funds were only used for legitimate business needs. Investors make their investments with the knowledge that their funds will be used for specified, stated goals; ultra vires actions run the risk of misappropriating funds and eroding confidence.

- To put it briefly, the doctrine: Prevents corporate power abuse.

- safeguards creditors and shareholders.

- respects the law in business dealings.

- guarantees accountability and openness in corporate governance.

Legal Basis under Indian Company Law

The Companies Act of 2013, specifically its implications in the Memorandum of Association provisions (Sections 4 and 6), recognises the Doctrine of Ultra Vires in India. While Section 6 declares any act that is in conflict with the Act or the Memorandum or Articles to be null and void, Section 4(1)(c) requires that the Memorandum clearly outline the company’s goals.

Therefore, a transaction is void ab initio and cannot be validated, even by unanimous shareholder consent, if a company goes beyond its object clause or engages in an activity that is beyond the scope of the Act.

Scope of the Doctrine

The doctrine’s broad application includes the following actions:

Ultra vires the business:

- Beyond the authority granted by the Memorandum.

- Beyond the directors’ authority but within the company’s powers is known as ultra vires.

Ultra vires the Articles of Association:

- Although the act is contained in the Memorandum, it does not comply with the Articles.

- Each has unique legal ramifications: actions taken outside the company’s authority are null and void.

- Shareholders may approve actions taken beyond the directors’ authority.

- By changing the Articles themselves, acts that go beyond the scope of the Articles can be justified.

- This distinction is important because it establishes whether or not a defect is curable.

Key Judicial Cases:

Let’s look at some landmark cases that shaped the evolution of the doctrine:

- Ashbury Railway Carriage and Iron Co. Ltd. v. Riche (1875) LR 7 HL 653

The doctrine’s foundational case is this one. The company’s goal was to manufacture and market railway carriages. Nonetheless, the directors signed a deal to finance the building of a railway line in Belgium. The House of Lords ruled that the contract was null and void because it went beyond the company’s authority. It was not even validated by shareholder approval.

The established principle states that any action that goes beyond the company’s objectives is null and void and cannot be approved.

- Great Eastern Railway Co. v. Attorney General (1880) 5 App Cas 473

The strictness of the doctrine was improved by this case. The court ruled against a narrow interpretation of ultra vires. An act is not ultra vires if it is reasonably incidental to the company’s primary goals. Activities that are “reasonably necessary” to accomplish the main goal are therefore acceptable.

Principle established: Acts incidental to the main objects are not ultra vires.

- Life Insurance Corporation of India v. A. Lakshmanaswami Mudaliar, AIR 1963 SC 1185

In this well-known Indian case, a company’s directors gave money to a charity trust that had nothing to do with the company’s operations. This act was deemed ultra vires by the Supreme Court because it was not in line with the company’s goals or helpful in achieving them.

The established principle states that corporate funds cannot be used for non-business-related purposes.

- 20 Ch D 169 Re German Date Coffee Co. (1882)

Here, the business was established to produce coffee alternatives using German-grown dates. It tried to move operations to a different location after that plan didn’t work out. The court ruled that the company could not alter its goals unless it was formally changed in accordance with company law procedures.

Established principle: A business must adhere to the parameters of its specified goals.

- 1 Ex D 88 Eley v. Positive Government Life Assurance Co. (1876)

This case showed that if an act is not included in the company’s statutory contract, it cannot confer enforceable rights and cannot conflict with the articles of association.

Consequences of Ultra Vires Acts

When an act is considered ultra vires, there are severe consequences:

- Void ab initio: The transaction is void from the start.

- Ratification incompetence: It cannot be validated by unanimous shareholder consent.

- Personal liability of directors: Directors who cause the company to act outside of its authority may be held personally liable.

- Injunctions: In order to stop an ultra vires act, shareholders may request an injunction.

- Restitution: To put parties back in their starting positions, restitution may be made if at all possible.

Relevance in Modern Company Law

The doctrine has changed with modernisation and legislative flexibility, despite its historical rigidity. Companies can now define their goals more broadly thanks to the Companies Act of 2013, which lowers the possibility that an action will be deemed to be beyond the bounds of the law.

In order to ensure corporate accountability, the doctrine is still relevant from a moral and legal standpoint. It continues to serve as a deterrent against corporate abuse and managerial excess.

The doctrine reminds companies that legal personality is not a license for unrestricted enterprise in a time when corporate endeavours are diversifying quickly. Maintaining adherence to corporate purpose is still a crucial component of good governance, especially in light of the increased scrutiny from investors, courts, and regulators.

Comparative Insight: UK and India

The Companies Act of 2006, which essentially eliminated the need for a detailed objects clause, greatly loosened the doctrine in the United Kingdom. Unless otherwise specified, companies are now presumed to have unrestricted objects.

India permits more flexibility while maintaining the core of the doctrine. Section 4(1)(c) still requires that objects be stated in the memorandum, but businesses are free to word their clauses however they see fit. However, in cases where an action manifestly goes beyond the statutory and Memorandum limits, the doctrine remains applicable.

Criticisms of the Doctrine

Despite having good foundations, the ultra vires doctrine has drawn the following criticisms:

- Application that is rigid: Even legitimate transactions that are advantageous to the business are rendered invalid by it.

- Commercial inconvenience: It limits the flexibility of businesses.

- Complexity: It can be challenging to determine if an act is ultra vires.

- Third parties may unjustly suffer if they are outside parties doing business with the company in good faith.

Therefore, by recognising implied powers and interpreting objects clauses liberally, modern corporate law has loosened the doctrine.

The Present Scenario

The business world of today prioritises pragmatic realism over strict formality. Rather than serving as an operational barrier, the ultra vires doctrine largely endures as a warning.

Indian courts now take a purposeful stance, making a distinction between acts that are genuinely unlawful and those that are merely incidental. The spirit of the doctrine has changed from one of punishment to one of protection, upholding corporate discipline, transparency, and trust.

Therefore, its real significance in contemporary practice resides in the caution it conveys: fiduciary responsibility has limits and corporate power is not limitless.

Summary Table: Ultra Vires in a Nutshell

Questions & Answers

- What is meant by Ultra Vires?

It denotes an action taken outside of the company’s authority.

- Can an ultra vires act be validated by shareholder approval?

No, even if they are unanimously approved, such acts are null and void.

- In what case was the doctrine first introduced?

Riche v. Ashbury Railway Carriage & Iron Co. Ltd. (1875).

- Does the Companies Act of 2013 still apply to the doctrine?

Yes, but because of more expansive object clauses, its practical significance has diminished.

- What would happen if directors committed acts that went beyond their authority?

They might be held personally responsible for paying back money or repairing any losses.

Final Thoughts: Staying Within the Lines

A pillar of corporate discipline is still the Doctrine of Ultra Vires. Even though contemporary company law is flexible, its fundamental principles of upholding honesty, responsibility, and legal governance remain relevant. This theory serves as a reminder that even ambition has its limits in a business environment that is characterised by expansion and innovation.

Because real power in law, as in life, comes from knowing your limits rather than acting outside of them.

Ayush Agrawal is a final year LL.B. (Hons.) student, with a background in Bachelor of Commerce. He has over 2 years of legal experience specializing in contract drafting, intellectual property, legal research, and client communication. Skilled in statutory interpretation, case law analysis, and managing confidential legal matters, Ayush is committed to supporting legal teams in civil, criminal, IP, and corporate law with accuracy, efficiency, and professionalism.